7 Ways to Maximize Your Military Benefits

Serving in the military comes with a wealth of financial benefits - but many service members and veterans don’t take full advantage of them. From securing a VA loan to saving for retirement or using education benefits, these programs can significantly improve your financial future. Here’s a quick overview of how to make the most of what’s available:

- VA Loans: Buy a home with no down payment and skip mortgage insurance.

- Thrift Savings Plan(TSP): Grow your retirement savings with low fees and government matching contributions.

- GI Bill: Cover education costs for yourself or transfer benefits to family members.

- Military Discounts: Save on shopping, travel, and everyday expenses.

- Tax Benefits: Reduce your tax burden with combat pay exclusions and PCS deductions.

- Extra Pay Opportunities: Earn more through special duty, hazardous duty, or deployment pay.

- Emergency Savings: Use programs like the Savings Deposit Program (SDP) for high returns.

Take action today by focusing on the benefits that align with your current goals. Whether it’s buying a home, planning for retirement, or saving during deployment, these programs are here to help you and your family thrive.

1. Get the Most from Your VA Loan Benefits

VA loans come with perks like no down payment and no monthly mortgage insurance, potentially saving you thousands of dollars. To make the most of these benefits, it’s essential to understand the process and choose the loan type that fits your needs.

Know Your Eligibility Requirements

To access a VA loan, you’ll need a Certificate of Eligibility (COE). The VA processes most COE requests electronically, with about two-thirds issued immediately. Eligibility depends on your service period and status. For instance:

- Active-duty service members typically qualify after 90 continuous days of service.

- Veterans who served from August 2, 1990, onward generally need 24 continuous months of active duty.

- National Guard and Reserve members may qualify with 90 days of non-training active-duty service or six creditable years in the Selected Reserve, provided they received an honorable discharge.

To apply, you’ll need service documentation, such as a DD Form 214 for veterans or a Statement of Service for active-duty members. Even if you’re unsure about meeting the requirements, it’s worth applying - special circumstances may still qualify you.

Once your COE is secured, focus on finding the loan type that aligns with your financial goals.

Pick the Right VA Loan Type

VA loans are versatile, offering options for various needs:

- VA Purchase Loan: Ideal for buying a primary home, this loan requires no down payment and often offers better terms than conventional mortgages.

- Interest Rate Reduction Refinance Loan (IRRRL): If you already have a VA loan, this option allows you to refinance to a fixed-rate mortgage, potentially stabilizing monthly payments.

- VA Cash-Out Refinance: Need funds for major expenses? This loan lets you access your home equity, even if you’re refinancing a conventional mortgage.

- VA Renovation Loans and Energy Efficient Mortgages: These loans combine the purchase price and the cost of home improvements or energy upgrades into one package.

Evaluate your financial situation and long-term objectives to choose the loan that works best for you.

Reduce or Skip Funding Fees

VA loans typically include a funding fee ranging from 0.5% to 3.3% of the loan amount. For example, a first-time VA loan user buying a $200,000 home with no down payment might pay a funding fee of around $4,300. However, there are ways to lower or eliminate this cost:

- Disability Exemption: Veterans with a service-connected disability - even a 10% rating - are exempt from funding fees.

- Seller Contributions: VA rules allow sellers to cover up to 4% of the home’s appraised value toward closing costs, including funding fees.

- Rolling Fees into the Loan: You can add the funding fee to your loan balance to conserve cash.

- Lower Fees for IRRRLs: Refinancing with an IRRRL often comes with a reduced funding fee, usually around 0.5%.

Additionally, shopping around with multiple lenders can help you find better fee structures, and some state or local programs may offer assistance with closing costs. By exploring these options, you can minimize upfront expenses and maximize your VA loan benefits.

2. Increase Your Thrift Savings Plan (TSP) Contributions

The Thrift Savings Plan (TSP) is a powerful retirement savings tool for military personnel, offering low fees and government matching contributions. By optimizing your TSP strategy, you can significantly grow your retirement funds while potentially lowering your current tax liability.

Traditional vs. Roth TSP: Which One Fits You?

Deciding between Traditional and Roth TSP contributions boils down to when you want to pay taxes - either now or later. Each has its own set of benefits depending on your financial situation and future plans.

"With traditional TSP, your contributions go into the TSP before tax withholding, which can potentially lower your current income tax rate. But when you take money from your traditional TSP, you'll pay taxes on both your contributions and earnings at the income tax rate of the year you make the withdrawal. With Roth TSP, your contributions go into the TSP after tax withholding...The advantage of the Roth TSP is that you won't pay taxes later when you take out your contributions and any qualified earnings."

- Traditional TSP: Contributions are pre-tax, reducing your taxable income now. However, withdrawals in retirement will be taxed, including both contributions and earnings.

- Roth TSP: Contributions are made with after-tax dollars, meaning you pay taxes upfront. The upside? Qualified withdrawals in retirement are completely tax-free.

For many service members, the Roth TSP can be a smarter choice. Why? Most are in a lower tax bracket now than they are likely to be in retirement. Financial advisor Lacey Langford, AFC®, explains:

"For most, the Roth TSP is the better choice because currently, you're in a lower tax bracket than you'll be in the future. With a Roth, your earnings and withdraws are tax-free because you contribute after-tax money, meaning you pay taxes upfront. So you won't have to pay taxes when you withdraw your money after 59 1/2 years old."

You can also split your contributions between Traditional and Roth TSP accounts for tax diversification. Keep in mind, though, that government matching contributions always go into your Traditional TSP account, regardless of how you allocate your personal contributions.

Once you’ve chosen your contribution type, make sure to adjust your contributions to take full advantage of the government match.

Maximize Your Government Match

Under the Blended Retirement System (BRS), the government offers matching contributions - essentially free money - but only if you contribute enough to earn it.

Here’s how it works: The government automatically adds 1% of your basic pay to your TSP, even if you don’t contribute anything. To get the full match, you need to contribute at least 5% of your basic pay each pay period, which unlocks the maximum government match of up to 5% total.

"To receive the maximum Agency/Service Matching Contributions, you must contribute at least 5% of your basic pay each pay period."

Timing is crucial. If you hit the annual TSP contribution limit ($23,500 in 2025) before the year ends, both your contributions and government matching will stop. For example, if you front-load your TSP contributions after receiving a bonus or deployment pay, you might max out by September and lose out on three months of matching contributions. To avoid this, use the TSP calculator on their website to figure out the right contribution amount per pay period.

For older service members, catch-up contributions offer an added opportunity. In 2025, those aged 50 and older can contribute an extra $7,500 on top of the standard limit. Additionally, service members aged 60-63 can make "super catch-up contributions" of up to $11,250, allowing a 60-year-old to contribute up to $34,750 total.

Simplify Investments with Lifecycle Funds

TSP Lifecycle Funds (L Funds) provide a set-it-and-forget-it investment option. These funds automatically adjust your portfolio as you approach retirement, shifting from a stock-heavy allocation to a more conservative mix of bonds. They spread investments across the five TSP core funds (G, F, C, S, and I) and are designed to align with your target retirement date.

Here’s how it works: Choose the L Fund that matches your expected retirement year. For instance, a 25-year-old planning to retire in 2065 would select the L 2065 Fund. Early on, these funds focus on growth by investing heavily in stocks, then gradually move toward bonds as the retirement date nears.

However, L Funds aren’t perfect. They don’t consider your personal risk tolerance, other investments, or unique financial goals. Some experts suggest that their automatic allocation across all five TSP funds might not be ideal for every investor .

Consider a Custom Allocation

If you prefer more control, you can build a custom allocation using just the C Fund (S&P 500) and G Fund (government securities). This simplified strategy has historically delivered higher returns compared to many L Funds while reducing complexity.

The choice between L Funds and a custom allocation depends on your comfort with managing investments. L Funds offer simplicity and automatic rebalancing, while a custom approach gives you the potential for better returns with more control over your portfolio.

3. Use GI Bill Education Benefits Fully

The GI Bill provides up to 36 months of education funding, but many service members miss the chance to fully take advantage of it. With some thoughtful planning, you can stretch these benefits further. Here are three ways to make the most of your GI Bill entitlement.

Make the Most of Your GI Bill: Transfer Benefits to Family Members

One standout feature of the Post-9/11 GI Bill is the option to transfer unused benefits to your spouse or children. This can provide financial flexibility for your family, much like optimizing your VA loan or TSP. To transfer benefits, you’ll need to initiate the process while still on active duty or in the Selected Reserve through milConnect. Also, ensure your dependents are registered in the Defense Enrollment Eligibility Reporting System (DEERS) to qualify.

Spouses can usually start using the benefits as soon as the transfer is approved. Children, however, may need to wait until you’ve completed 10 years of service and meet certain age or education criteria. Keep in mind that spouses don’t qualify for the monthly housing allowance while you’re on active duty, but children might. You retain control over the transferred benefits until they’re used, but there’s a catch: transferring benefits requires a service commitment, and failing to meet it could result in the VA reclaiming benefits already used by your family.

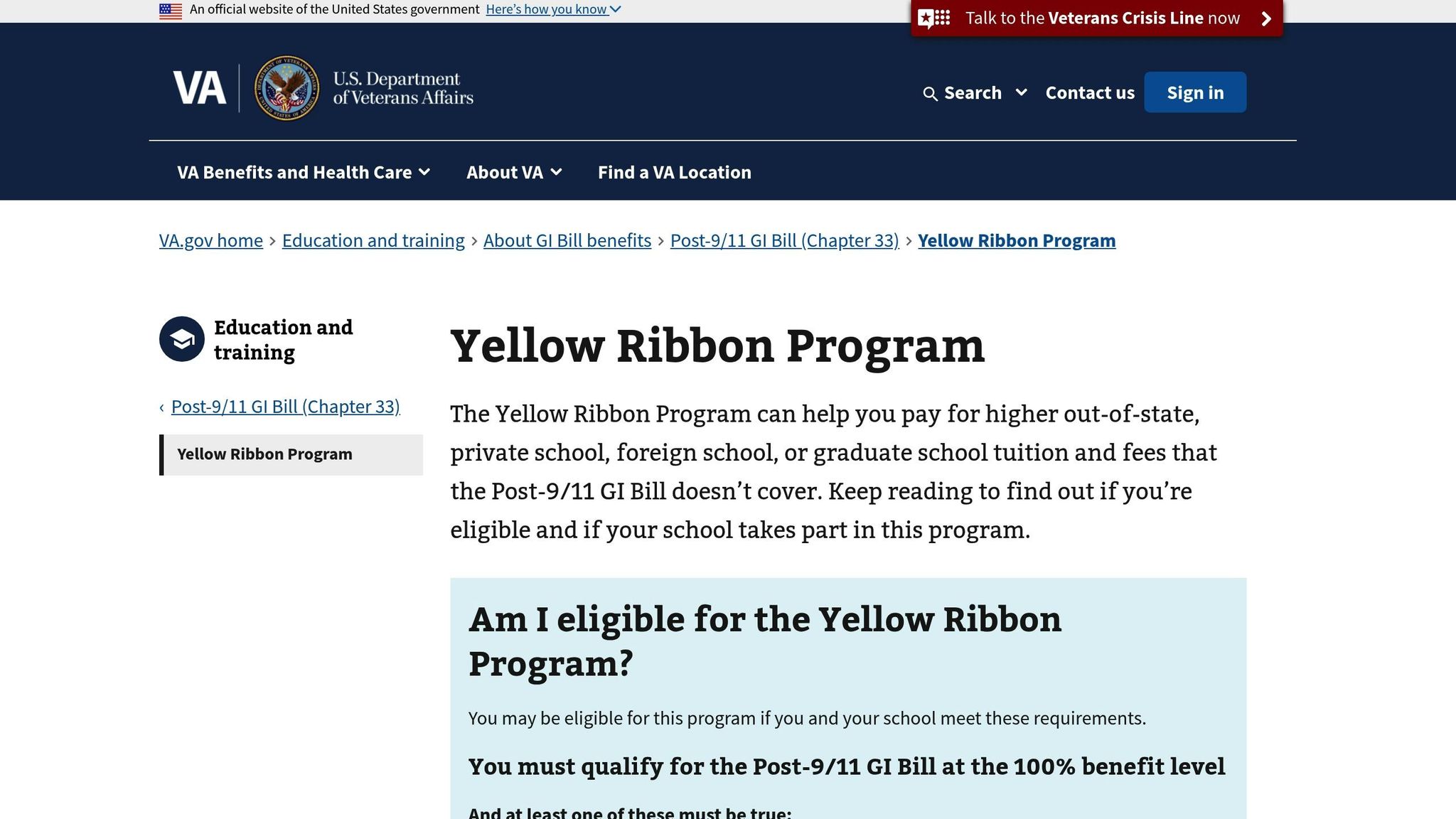

Make the Most of Your GI Bill: Combine It with the Yellow Ribbon Program

The Yellow Ribbon Program can significantly increase your education funding, especially if you’re attending a private school or studying out-of-state. This program is available to those eligible for 100% Post-9/11 GI Bill benefits and works by matching contributions from participating schools to cover costs that exceed standard limits. For example, in the 2024–2025 academic year, the maximum Post-9/11 GI Bill payment for private schools is $28,937.09. If tuition exceeds this amount, the Yellow Ribbon Program helps cover the difference.

Here’s how it works: if a school contributes a set amount, the VA matches it dollar-for-dollar. This funding applies to tuition and fees at private institutions, foreign schools, and public schools for out-of-state students. However, it doesn’t cover room and board, study abroad programs, or penalty fees.

Not all schools participate, and some may limit the number of students or funding available. Researching participating schools early in your decision-making process is crucial. Once approved for Yellow Ribbon benefits, you’ll continue receiving them as long as you maintain academic progress, stay enrolled, and have remaining GI Bill entitlement. If you transfer to another school, you’ll need to reapply for Yellow Ribbon funding.

Make the Most of Your GI Bill: Use Benefits Strategically

Careful planning can help you maximize your 36 months of GI Bill entitlement and even save some for future use or transfers to family members. One way to do this is by opting for accelerated programs - many schools offer year-round classes, summer sessions, or intensive formats that help you complete your degree faster and conserve your benefits.

Consider focusing on fields that align with your military experience and offer strong career prospects, such as cybersecurity, healthcare, technology, or project management. These areas often provide a good return on investment and may even allow you to earn credit for relevant military training.

To get started, gather the necessary documents and apply online through the VA website. The VA’s GI Bill Comparison Tool can also help you estimate your benefits at different schools, enabling you to make informed choices.

If you’re eligible for more than one GI Bill program, remember that choosing the Post-9/11 GI Bill is a permanent decision. Consult your school’s certifying official to ensure you’re making the best choice for your situation.

4. Use Military Discounts and Perks

Serving in the military opens the door to exclusive discounts and travel perks that can help stretch your paycheck and build financial stability for you and your family.

Save Big at the Commissary

Shopping at the commissary can save you about 25% compared to regular civilian stores. While there is a 5% surcharge that goes toward store improvements, you’ll avoid paying sales tax, which adds up to significant savings.

To get the most out of your commissary trips, sign up for their newsletter to stay updated on sales. You can also take advantage of additional savings through Maxi Saver Coupons, Military Shoppers Flyer, My Military Savings, and SmartSource Coupons. By planning your shopping around sales and stacking coupons, you can make every trip to the commissary a money-saving win. These savings can free up funds for other perks like affordable travel and exclusive retail discounts.

Take Advantage of Space-Available Travel

Space-Available (Space-A) travel offers free or low-cost flights on military aircraft, making it an amazing option for those with flexible schedules. Although there are small fees, they’re a fraction of what you’d pay for commercial flights. Check with your local terminal for the latest fee information.

Before you travel, contact the terminal to confirm procedures. Many terminals post updates on their Facebook pages, which can help you plan more effectively. For international trips, ensure you have your DoD ID, a valid passport, and a recent negative COVID-19 test. Flexibility is essential - be prepared to adjust travel dates or destinations and have a backup plan for lodging or transportation in case Space-A travel isn’t available.

Find Discounts Everywhere

Military discounts aren’t just limited to Veterans Day - many retailers, restaurants, and service providers offer them year-round. These discounts often apply to active-duty members, veterans, retirees, reservists, National Guard members, and sometimes even their families. Always carry your military ID and ask about available discounts when shopping in-store.

For online verification, consider creating an ID.me account. As ID.me explains:

"ID.me helps you prove your identity across multiple websites. It serves the same purpose as the physical ID cards you carry in your wallet - but for the internet."

Retailers like Lowe’s have partnered with ID.me to provide military members with a 10% discount on most full-price items. In 2025, Lowe’s also offers a free Silver Key status upgrade for MyLowe’s Rewards members, which includes free standard shipping and bonus reward points. Military spouses can access these perks by setting up their own ID.me account. Other companies, like uShip, also use ID.me to offer exclusive promotions for active-duty members, veterans, retirees, and their spouses.

For even more options, download apps like VetsApp, which helps veterans manage benefits, access discounts, and stay informed about resources. You can also visit websites like Military.com’s Discount Center or the ID.me Shop to explore a wide variety of military discount opportunities.

5. Use Your Tax Benefits

In addition to managing loans and savings, understanding tax benefits is a key part of making the most of your military financial resources. Military service comes with several tax perks that can save you thousands of dollars each year.

Combat Zone Tax Exclusion (CZTE)

If you're on active duty in a designated combat zone, you may be eligible to exclude your combat pay from taxable income. To qualify, you need to be actively serving in a designated combat area and present there for any part of a month. The Department of Defense Financial Management Regulation (FMR) Volume 7A, Chapter 44, Paragraph 440203 provides a list of these zones.

For enlisted service members and warrant officers, the exclusion is unlimited. For commissioned officers, it's capped at the maximum enlisted pay plus Hostile Fire or Imminent Danger Pay. As of March 2025, this amounts to $10,294.80 in basic pay plus $225 per month for Hostile Fire Pay.

Jeff Jurgemeyer, a CFP® with over three decades of experience and multiple deployments, highlighted this benefit in April 2025:

"It's one of many financial perks of serving in a combat zone, allowing you to keep more of your hard-earned pay because all (or most) of your pay is tax-free."

To ensure you receive this benefit, keep records of your orders and Leave and Earnings Statements (LESs). If your W-2 doesn’t reflect the combat zone exclusion, contact your military pay office for a corrected form. Additionally, the IRS gives you an extra 180 days to file your taxes after your last day in a combat zone. Another advantage is the increased Thrift Savings Plan (TSP) contribution limit, which rises to $70,000 in these zones.

State Residency Tax Planning

Choosing the right state for your legal residency can significantly reduce your state income tax burden. Thanks to the Servicemembers Civil Relief Act (SCRA) and the Military Spouses Residency Relief Act (MSRRA), you can maintain your state of legal residence (SLR) even when stationed elsewhere. For tax purposes, your SLR remains your primary domicile no matter where you're posted.

Opting for a state with no income tax - like Florida, Nevada, or Texas - can be particularly beneficial. States such as Florida, Nevada, South Dakota, Texas, Washington, and Wyoming do not impose any state income tax. Additionally, as of July 2024, several other states offer military income tax exemptions under certain conditions. For example, Alaska, Illinois, Iowa, Michigan, Missouri, North Carolina, Ohio (if stationed outside the state), and Pennsylvania (if stationed out of state) provide such exemptions.

The 2023 Veterans Auto and Education Improvement Act of 2022 expanded options further. Active-duty service members and their spouses can now choose one of three bases for filing state income taxes: the service member's residence, the spouse's residence, or the service member's permanent duty station. Be sure to update your driver's license, vehicle registration, and voter registration to align with your chosen state. Spouses should also explore their options under MSRRA.

Want More Value?

Check out exclusive offers, tools, and resources curated for military members and their families.

Explore Exclusive Offers